Who has enough income, enough desire, and just the right demographic profile to buy furniture and home accessories right now? The Henry’s do!

As a girl I discovered Nancy Drew, the young reader’s detective series by mystery writer Carolyn Keene. I was hooked on the mystery genre. So I graduated to Sherlock Holmes and Agatha Christie, then onto other mystery writers, preferring the British authors like Dorothy Sayers, Ngaio Marsh, Josephine Tey, Ellis Peters, and P.D. James. Also Elizabeth George, though she is an American, her mysteries are set in the U.K. and follow the traditions of the British greats.

I’ve often thought career-wise, I missed my true calling – to be a real-life detective. Yet as a market researcher, I’m just about the closest thing you can get to it, without having to deal with the blood, gore and guts of real detective work.

Mystery-novel enthusiasts and police procedural fans know that detectives investigate a crime and identify the criminal by focusing on these three aspects:

- Means – Who had the means to commit the crime?

- Opportunity – Who had the opportunity to commit it?

- Motive – Most importantly, who had a reason to do it?

A market researchers’ job is to understand customer behavior and identify the best potential customers. That takes detective work, which means uncovering who has the means, opportunity and motive to buy goods and services. The same three perspectives apply to researching a new consumer market segment.

HENRYs Have the MEANS to Buy

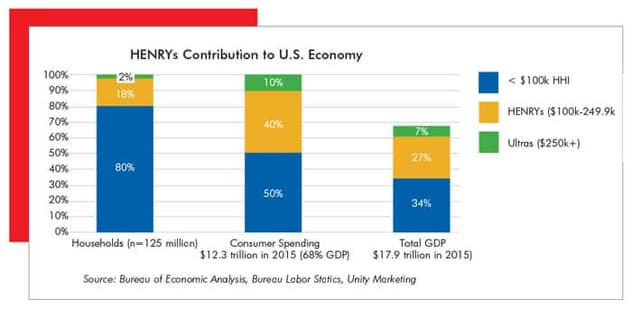

The key to identifying customers with the means to buy home furnishings is to understand the demographics of HENRYs (High Earners, Not Rich Yet).

Demographics provide the facts and figures that allow marketers to zero in on the best prospects. Income, gender and increasing age demographics best define the HENRYs, particularly younger HENRYs, as home marketers’ best new customer prospects.

The HENRYs term was originally coined by Shawn Tully in a 2003 Fortune magazine article focused on the segment’s heavy tax burden. But for home marketers, their spending potential is primary.

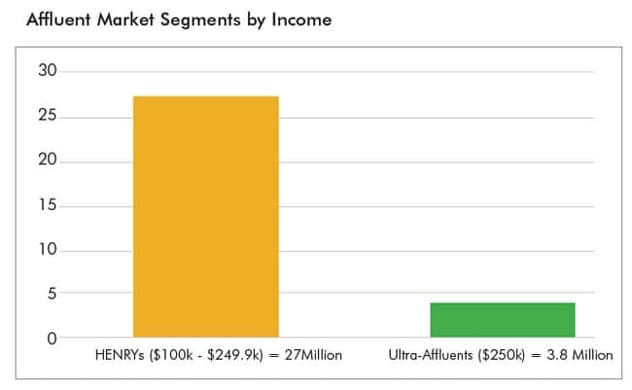

Unity Marketing defines the affluent as those with household incomes at the top 20% of the U.S. overall. HENRYs are defined by their income, ranging from $100,000 to $249,000.

Younger HENRYs

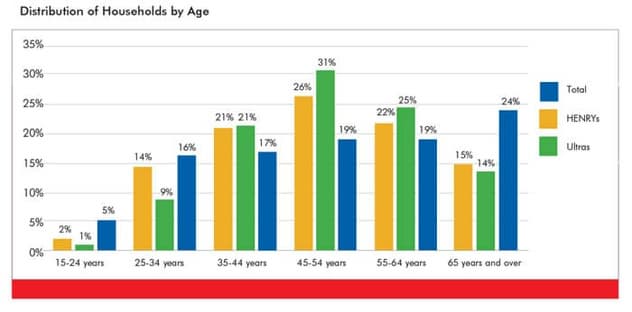

Affluence comes with middle-age, with income peaking from age 35-54 years, after which people start to retire, which tends to drive down the overall income of those from age 55-64 years. So for both HENRYs and Ultra-affluents the ages of 45-54 years specifically are when both segments’ peak in terms of size and spending power.

However, HENRYs are far more heavily represented in the younger age ranges, 24-34 years than Ultra-affluents. These younger HENRYs are busy growing in their careers and incomes.

In Unity Marketing’s affluent tracking study, $250k marks the line between mass affluence and ultra-affluence. Additionally, two key age ranges, 24-44 years (young affluents) and 45-64 years (mature affluents), have emerged as significant to marketers aimed at the high-end and luxury segments.

Those in the young affluent segment are significantly more active purchasers of luxury goods and services, especially home furnishings, as they are in an acquisitive life stage, forming families, establishing households, buying homes and investing in luxuries to enhance their lifestyles. Mature affluents, 45 to 64 years, have already acquired many goods that define a luxury lifestyle. They are transitioning out of an acquisitive mindset toward a more experiential one, often downsizing their homes as children leave the nest and their housing needs change.

This is not to say that mature affluents, including mature HENRYs, don’t represent an important market segment for home marketers, but younger HENRYs, aged 24-44 years, are primed for buying things to decorate and enhance the quality of their lifestyles in the home. As a result, home brands as diverse as IKEA, RH, Pottery Barn, Crate & Barrel, West Elm, Ethan Allen and others have found success focusing on the luxury leanings of young HENRY affluents.

Gender is Less Important Than HENRYs Marital Status

In certain marketing categories, gender plays a decisive role; however, in home-related purchases, especially among the affluents, marital status is far more important. That’s because the vast majority of affluents, both HENRYs and Ultra-affluents, are married and largely make home decisions as a couple. Indeed marital status is a key demographic distinctive in the affluent market, since often it takes two incomes to propel a household into the top 20%.

As compared with the U.S. population as a whole where only two-thirds live in family households and one-third live in non-family households, over 80% of affluents, 78% of HENRYs and 83% of Ultra-affluents, live in a married-couple household. While HENRYs are slightly more highly represented in non-family households than Ultra-affluents, the differences are not statistically significant and can be understood by the higher representation of younger, still single affluents in the HENRY income segment.

Therefore, home marketers aiming to capture the spending power of HENRYs, need to be focused on the needs of young couples and growing families. That is the thinking behind Ethan Allen’s recent licensing partnership with Disney for a line of kid and youth furnishings.

High Levels of Education, a Demographic Distinctive

A final distinctive defining the HENRY consumer is high educational attainment. While only about one-third of all U.S. households are headed by a consumer with a college education, twice as many HENRYs and Ultra-affluents (about 66%) have attained a college degree or post-graduate education. This means that home marketers can approach the HENRYs and communicate with them at a higher, more conceptual, value-focused level than can marketers aimed at more middle-income consumers.

Final word of advice, given the HENRYs high levels of income, educational attainment and career focus, HENRYs often have budgetary responsibilities in their jobs. They are trained and have experience evaluating purchasing options and making budgetary decisions that maximize the return on investment in spending. They seek out and know how to identify the purchase options that represent the best value for their companies.

When they go home at night, HENRYs don’t leave their business smarts at the office. They apply the same due diligence in making personal purchase decisions. HENRYs know how to measure meaningful value and will seek out the best options to deliver value at the most reasonable cost.

That calls on home marketers to communicate value messaging to HENRYs who aren’t necessarily interested in the cheapest option. They would rather find the most cost-effective products and services that deliver what they value and desire.

Young HENRYs Are Primed For Home-Related Products

Assessing your marketing opportunity with HENRYs requires understanding his or her shopping and purchase behavior. Consumers are more or less creatures of habit who tend to follow similar paths to purchase; ones that have worked successfully for them in the past.

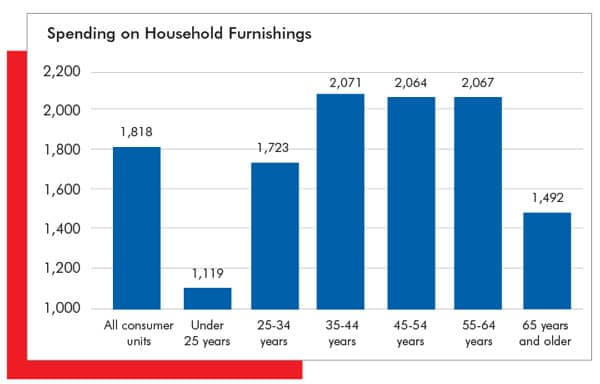

The Bureau of Labor Statistics Consumer Expenditure survey, the nation’s authority on consumer spending and the source used by policy makers in the federal government, identifies two key consumer segments where expenditures on household furnishings and equipment peaks: ages 34-44 years and household incomes over $100,000.

Admittedly, spending on home furnishings continues strong for those aged 45-64 years and peaks as incomes rise over $100,000, but since almost all of tomorrow’s Ultra-affluents start out as young HENRYs, these are the best customers for home marketers to make a connection today that can lead to growth and prosperity tomorrow.

Connecting with younger HENRYs is even more vital for home marketers’ strategy because as they mature, HENRYs’ housing needs are likely to change. From 25-34 years young people are in the household formation stage, starting their families and often buying their first homes. From 35-44 years they are likely to move up to a second home and add family members. In the mature life stages, from 45-64 years, consumers also make predictable changes in their homes as they perhaps move up again, or invest in a second home. Then as children leave the nest and retirement approaches, they may move again to a smaller home, all the while continuing to have the need for new home furnishing and home decorating solutions.

To dig even deeper into young HENRYs purchasing and shopping behavior, syndicated market research studies can provide more insight. For example, Unity Marketing measured two independent but important variables that are key indicators of affluent purchase behavior in the home furnishings space:

- Luxury home furnishings demand – which indicates the percentage of affluents, both HENRYs and Ultra-affluents, that made a recent purchase of home luxury goods.

- Luxury home furnishings spending – the amount of money spent making those home goods purchases across nine different categories, including furniture, floor coverings, outdoor luxuries, home electronics, decorative home accents and tabletop, linens and other soft goods, art and wall décor, major home appliances, kitchenware and housewares, and mattresses and sleep systems.

Included in those studies are the specific types of products bought in each category and where purchases were made. Here are highlights of recent Unity Marketing studies.

Growing Demand

Statistically, there is no difference between the percentages of HENRYs and Ultra-affluents that make home goods purchases.

65 per cent of all affluent households purchased home luxury goods in 2016. That being said, it is important to recognize that with a population of 27 million people, far more Henry’s purchased luxury goods than Ultra Affluents (population 3.8 million).

The home luxury market is deeper, wider and bigger among the lower-income HENRYs than the Ultra-affluents, who tend to be the primary targets of traditional home luxury brands. HENRYs represent a huge potential opportunity for home marketers.

Ultra Affluents Spend Less

While demand may be equal between the two affluent segments, the same cannot be said for spending. Ultra-affluents with their far greater income and wealth spend more on home luxury goods, though the differences in spending between HENRYs and Ultra-affluents has been narrowing. Unity Marketing data shows that Ultra-affluents are starting to spend more like HENRYs.

The survey reveals that spending on home luxuries declined almost a third from 2012 to 2016, even while demand for home luxuries increased over the same five-year period.

This pattern -- demand on the rise, but spending on the decline -- indicates that the affluents are spending less on more purchases. Affluent consumers are buying at a discount, trading down to less high-end brands, selecting less expensive options (e.g. choosing accent pieces and fewer major furniture pieces), and/or economizing in other ways.

Shopping Patterns Shift

Disruption is a favorite word pundits use when talking about how consumers are shopping differently than they did in the past. While big national retailers, such as Macy’s, JC Penney’s and Sears are closing stores, other retailers, notably RH, are opening grander stores that offer new shopping experiences.

And then there is the internet. Amazon continues to expand its merchandise assortment to offer more and better things for the home, and Wayfair, with its family of online brands, including Joss & Main, AllModern, Dwell Studio and Birch Lane, has grown from sales of a mere $601 million in 2012 to $2.25 billion in 2015. Net revenues for the first two quarters of 2016 are up 76.1% in 1Q16 and 60% in 2Q16 over previous year periods.

All in all, affluents today have a much wider range of home products to buy and places to buy them than they did a mere two years ago. Unity Marketing’s Affluent Consumer Tracking Study (ACTS) tracks where HENRYs, as well as Ultra-affluents, make their purchases in nine different home product categories. It reveals these as the fastest growing channels for shoppers within each category.

Nine Growth Categories

1. Art & Antiques. While art galleries remain HENRYs go-to destination for art purchases, specialty home furnishing stores, department stores, and discount stores, outlets and warehouse clubs are among the fastest growing destinations to purchase art and wall décor.

And while the internet ranks second as HENRYs’ shopping destination for art and wall décor, it isn’t growing as fast as home furnishings, department and discount stores. This may signal that internet shopping, at least for art and wall décor, is reaching its peak.

2. Home Electronics. For this category of goods, specialty electronics stores remain the destination of choice, but more HENRYs are also sourcing their television sets, audio systems and other home electronics from online retailers. To date discounters, outlets and warehouse clubs haven’t made significant strides in capturing the spending of affluents in this category.

3. Furniture, Lamps and Floor Coverings. Specialty home furnishings stores are the destination of choice for HENRYs when shopping for these goods, though their use of the internet has more than doubled since 2013 and home improvement store purchases have increased by 77%. These shifts make internet and home improvement stores the second and third most important destination for these goods. Of note, use of interior designers as a source for these goods declined from 13% to only 5% of affluent shoppers.

4. Garden, Outdoor and Patio. Garden centers and big-box home improvement stores capture the bulk of HENRY shoppers in this category, but art galleries that offer more artistic, hand-crafted items for the garden and patio are a rapidly growing source for these goods. Also trending are specialty home furnishing stores and discounters, outlets and warehouse clubs as a source for HENRYs’ garden decorating needs.

5. Kitchenware, Cookware and Housewares. The HENRYs’ top three most important shopping destinations in this category are specialty gourmet cooking stores, internet and department stores, in that order. Except for a growing use of the internet for these purchases, there hasn’t been any other significant shift in shopping patterns.

6. Major Appliances, plus Bath Fixtures and Building Products. An important category for many luxury appliance and fixture companies, the HENRYs have been moving toward home improvement stores and the internet for these purchases. They are less likely to frequent specialty appliance dealers and interior designers/contractors for these purchases.

This suggests to brands that strictly limit distribution to designers and appliance dealers that they may want to broaden distribution to less exclusive channels in order to connect with high-potential HENRYs.

7. Linens & Bedding. Department stores are the primary shopping destination for HENRYs when looking for home linens, and since 2013 department stores have grown even more as a primary destination. Also posting growth in this category is luxury-branded boutiques and discounters, outlets and warehouse clubs. Interestingly, the internet reached a peak in 2014 but recently dropped back to 2013 levels.

8. Mattresses & Sleep Systems. The internet is the big news in the change in where HENRYs are shopping for mattresses and sleep systems. Use of the internet for these purchases has doubled since 2013, to be the second most popular destination.

Internet growth came at the expense of lost patronage in mattress specialty and furniture stores, though mattress specialty stores remain the number one destination.

9. Tabletop, Flatware, Dinnerware, Glassware. Unlike other home categories, there is no clear winner as number one shopping destination for HENRYs when it comes to tableware. They shop widely across a range of stores, notably department stores, internet, specialty gourmet and tabletop stores, and specialty home furnishings stores, with the latter two growing in importance from 2013.

Overview

For each brand and each marketer their distribution strategies will necessarily differ. It makes sense to expand distribution in the fastest-growing channels. Yet, as is the case in art and linens and bedding, the internet may well be reaching its peak. So, moving aggressively to online distribution in these categories may not be the optimum strategy.

A key for any home marketer aiming to capture the HENRYs attention and spending is to:

- Not be too exclusive. Exclusivity to HENRYs feels undemocratic and too elitist, qualities that turn off more HENRYs than they attract. Your brand doesn’t need to be everywhere, but it needs to be accessible and affordable.

- Find partners that understand what value means to HENRYs. Above all, HENRYs are looking for value when it comes to purchases for their home. Not necessarily the cheapest offer, but the one that offers the best value for the money. That means, pricing is not about how low can you go, but how much value can you offer.

- Focus on “how” you sell. The key to success in retailing today is not about WHAT you sell, but HOW you sell it. Make sure your retailing partners believe the same thing and are willing to focus on the customer, their needs, desires and values in the retailing experience.

Furniture World is the oldest, continuously published trade publication in the United States. It is published for the benefit of furniture retail executives. Print circulation of 20,000 is directed primarily to furniture retailers in the US and Canada. In 1970, the magazine established and endowed the Bernice Bienenstock Furniture Library (www.furniturelibrary.com) in High Point, NC, now a public foundation containing more than 5,000 books on furniture and design dating from 1620. For more information contact editor@furninfo.com.